关于报告

A record number of new oncology drugs has been approved in recent years, bringing new treatment options to patients. However, despite robust levels of pipeline activity, oncology remains a challenging area for research and development. This report examines the productivity and output of the oncology pipeline, new treatment mechanisms, and which patients will likely benefit from new therapies. Our research brings into focus the amount spent on oncology medicines globally, clinical trial activity, complexity and success, and the outlook through 2023. The report also addresses shifts in therapy use with the emergence of immuno-therapies, Next-Generation Biotherapeutics and biosimilars.

Report Summary

A record 15 new oncology therapeutic drugs were launched in 2018 for 17 indications. Over half of the new therapies are delivered as an oral formulation, have an orphan indication or include a predictive biomarker on their label. Recently introduced therapies are also being used more broadly across varied tumor populations and in earlier lines of therapy. The use of immuno-oncology therapies has doubled in the United States since 2017 and treatment with novel CDK 4/6 inhibitors for HER-2 negative breast cancer has dramatically increased in the United States and Europe.

后期发育中的药物管道仅在2018年就扩大了19%,自2013年以来为63%。在管道和临床开发的所有阶段中,最激烈的活动集中在近450个免疫疗法上,具有60多种不同的作用机制。98个下一代生物治疗剂(定义为细胞,基因和核苷酸疗法)也在临床研究中,并利用18种不同的方法。

Despite high levels of pipeline activity, oncology remains one of the most challenging areas for research and development, facing significant risk of failure and long development times. The composite success rate for phase transitions fell to 8.0% in 2018 from 11.7% in 2017, and clinical trial duration remains higher for oncology trials than other disease areas. Clinical trial complexity has also increased sharply for phase I oncology trials over the past five years. The overall productivity of oncology trials – measured as success rates relative to trial effort (complexity and duration) – has improved by 22% since 2010 but remains far lower than trials for other therapy areas.

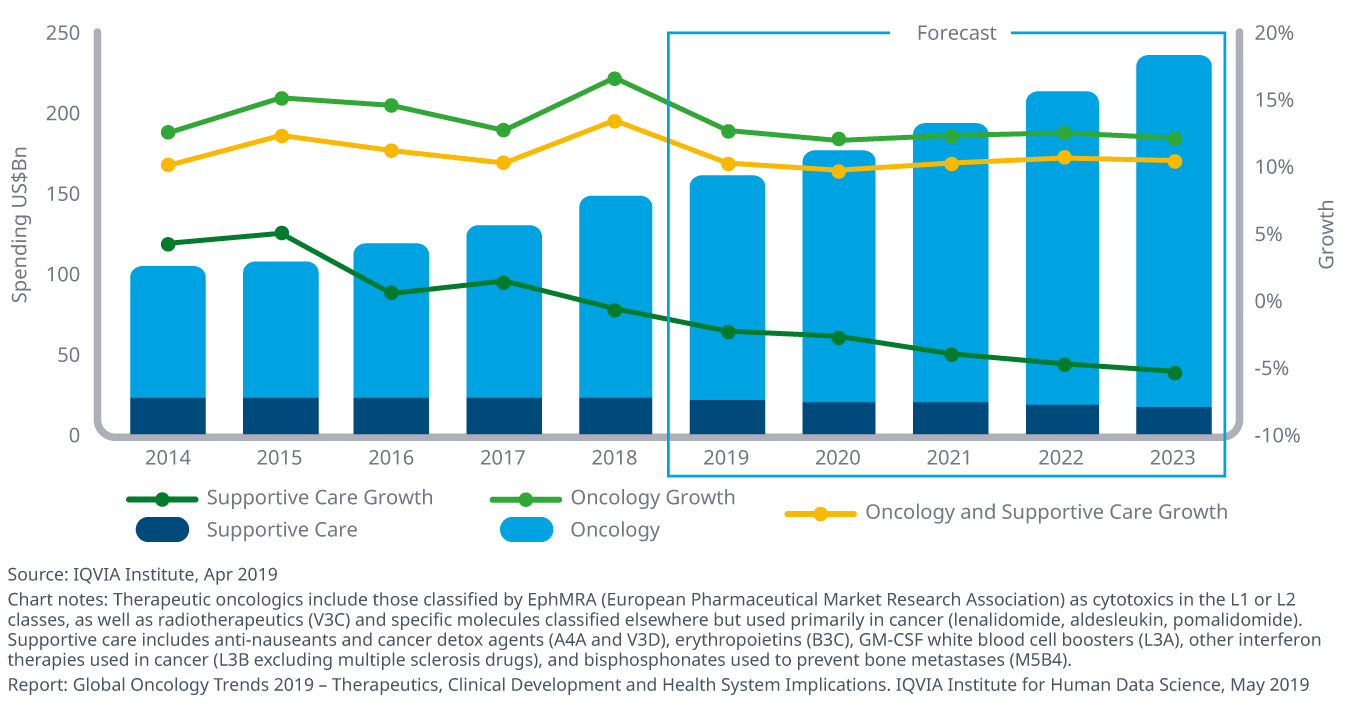

用于治疗癌症患者的所有药物的支出在2018年达到了近1500亿美元,这一年度增长了12.9%,并标志着连续第五年的双位增长,这完全由治疗药物驱动,该药物的增长15.9%。新药物的平均每年成本继续趋势上升,尽管中位成本在2018年下降了13,000美元,至149,000美元,而每种产品的成本范围为90,000美元,超过30万美元。中国领导了药房的支出和增长市场,在2018年增长了24%,达到了90亿美元的总支出,即使中国的支持性护理治疗下降了10%。在接下来的五年中,预计将以复合年增长率将治疗性支出增长11-14%,使总市场达到200-23.33亿美元。

Key Findings

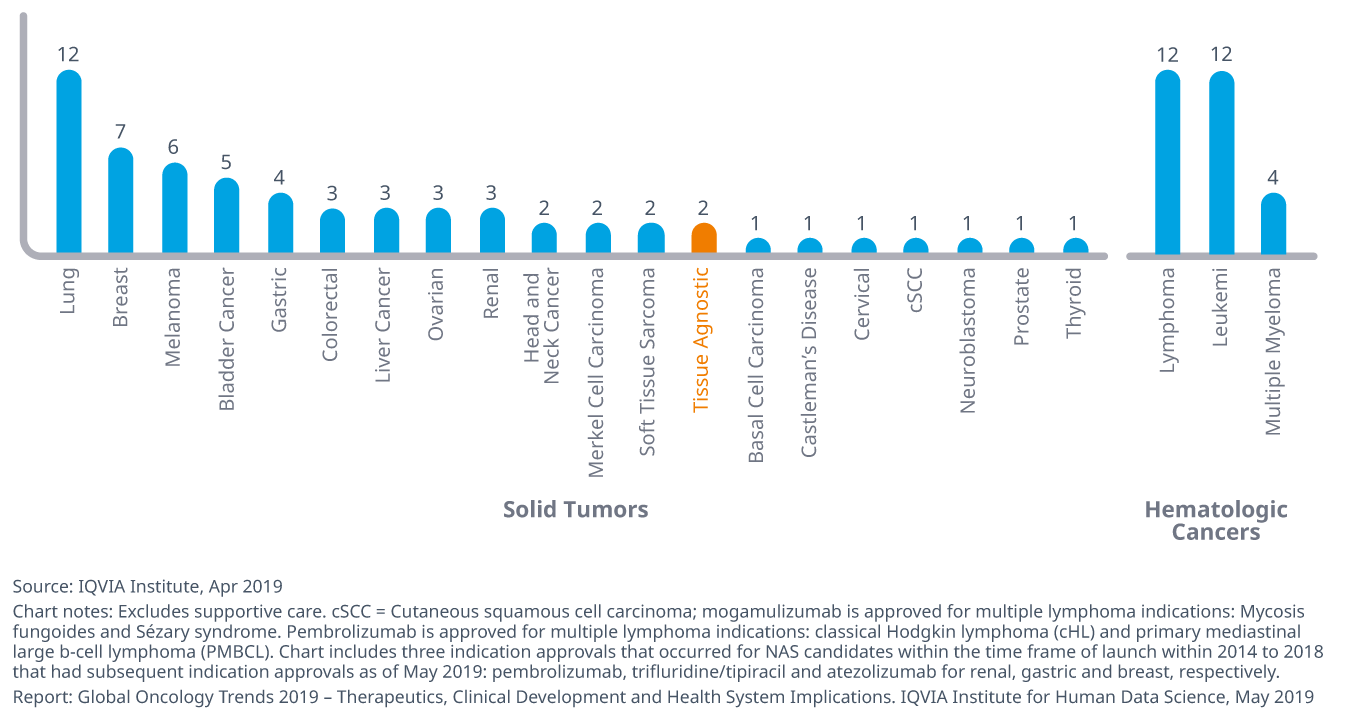

Over the past five years, 57 newly launched oncology therapeutics received approval for 89 indications, with some drugs treating multiple tumor types

- A record number of new oncology drugs was launched in 2018, bringing new treatment options to patients and continuing the transformation of treatment patterns occurring from the introduction of immunotherapies less than five years ago.

- Almost one-third of the approved indications over the past five years have been for hematologic cancers while lung cancer leads the solid tumors with 12 indications, followed by breast cancer and melanoma.

- In 2018, larotrectinib became the second tissue-agnostic oncology therapy to be approved, following the first approval of pembrolizumab in 2017. This reflects the beginning of a paradigm shift occurring in oncology to treat tumors based on genetic profile rather than site-of-origin in the body.

The late-stage oncology pipeline included 849 molecules in 2018, up 77% since 2008, due to the increasing number of targeted therapies

- The number of late-stage pipeline therapies grew from 711 in 2017 to 849 in 2018 – an expansion of 19% – due to the growing number of targeted therapies in the oncology pipeline.

- 91% of the late-stage oncology pipeline in 2018 were targeted small molecule and biologic therapies, rather than non-specific therapies like cytotoxic agents.

- The increasing numbers of medicines in the pipeline is particularly notable because of the range of mechanisms being explored, the numbers of companies involved and the rate at which the research is progressing.

- In late-stage oncology R&D, 711 companies are active, working on a total of 849 products, with the majority (88%) from emerging biopharma companies.

Almost 100 Next-Generation Biotherapeutics are now in late-stage development

- 自2013年以来,肿瘤学的开发中定义为细胞,基因和核苷酸疗法的下一代生物治疗剂的数量已增加了一倍以上,并且从2017年到2018年增长了32%,随着疾病治疗的新途径和治疗途径不断增长。。

- Nearly 450 immuno-oncology therapies are currently in development across all phases, with the Phase III and pre-registration pipeline containing nine mechanisms and the early- stage pipeline containing 62 mechanisms.

- PD1/PD-L1 checkpoint inhibitors remain the most successful immuno-oncology therapies, and improvements in formulation (e.g., oral) or immunotherapy combinations with targeted therapies (e.g., TKIs) or Next-Generation Biotherapeutics may lead to therapy breakthroughs.

Oncology clinical trials have a high risk of failure with a composite success rate of 8% in 2018, slightly lower than the average since 2010

![]()

- 自2013年以来的肿瘤产品以来,综合成功率衡量了进入I阶段的可能性,该产品将进入市场,而2015年和2017年的肿瘤学产品差异大致相同,而差异在7-8%之间。2010 - 2018年的总体平均水平为10.6%。

- 在所有试验阶段,2018年的肿瘤学试验的平均持续时间为3。2年,而其他所有治疗领域的平均持续时间为1。8年,差异超过40%。

- Clinical trial complexity in oncology has risen 11% from 2014 to 2018 and 22% from 2010 to 2018 and is being driven by increases in the number of endpoints and eligibility criteria and offset by declines in the number of countries and number of sites included.

建模当前临床发展趋势对未来生产率的影响,预筛查患者和生物标志物测试的可用性分别提高生产率,分别提高到2023年,分别提高了104%和71%。

- Overall productivity of oncology trials – measured as success rates relative to trial complexity and duration – has improved by 22% since 2010 but remains far lower than trials for other therapy areas.

- The most impactful trend in oncology development is expected to be the availability of pre-screened patients, to assess eligibility for trials and enhance the speed and efficiency of trials.

- Biomarkers continue to be discovered, both as a result of drug discovery and through other research, and the wider range and availability of tests will significantly enhance all aspects of drug development.

到2023年,肿瘤学支出将达到近2400亿美元,增长9-12%

- Spending on all medicines used in the treatment of patients with cancer reached nearly $150 billion in 2018 up 12.9% for the year, driven by therapeutic drugs, as spending on supportive care drugs declined 1.5% in 2018.

- The average annual cost of new oncology medicines continues to trend up, although the median cost dropped $13,000 in 2018 to $149,000.

- Oncology spending in China has more than doubled in the past five years, mostly coming from increased use of existing branded medicines, and very little from newly launched medicines and per capita spending in China amounts to $4.50 per person, compared to $173 in the United States.

- Growth in spending on oncology therapeutics through 2023 is forecast at double-digit levels in the United States, pharmerging markets and rest-of-world, will reach the high single-digit growth in the EU5, and 5–8% in Japan.